What is haulage insurance cover? A UK operator’s guide

Haulage insurance cover is a specialised package of policies designed to protect road freight businesses against the distinct risks of carrying goods commercially, including vehicle damage, cargo loss, third-party injury claims, and employer liability. Unlike standard commercial vehicle insurance, haulage cover addresses the full operational exposure of a freight business. Under the Road Traffic Act 1988, HGV motor insurance is a legal requirement for any vehicle used on UK public roads. The Employers’ Liability (Compulsory Insurance) Act 1969 adds a further mandatory layer for any business with staff. Understanding what is haulage insurance cover means understanding how these components combine into a single, coherent protection framework.

What does haulage insurance cover and what are its core components?

Haulage insurance is a combined insurance package built around the specific risks that freight operators face every working day. It goes well beyond insuring the vehicle itself. The core components address vehicles, cargo, and the legal liabilities that arise from operating heavy goods vehicles on public roads and at customer sites.

The principal elements of a haulage insurance package are:

- HGV motor insurance: Legally required under the Road Traffic Act 1988. Covers vehicle damage, road traffic accidents, and third-party injury or property damage caused by your vehicles.

- Goods in Transit (GIT) insurance: Covers loss, damage, or theft of customer goods while in your care, including during loading, unloading, and storage in transit. Coverage can extend to theft, accidental damage, fire, and loading-related damage.

- Public liability insurance: Covers claims made against your business for injury to third parties or damage to their property arising from your operations. Public liability limits in UK haulage range from £1 million to £10 million depending on operation type, with limits often driven by customer contracts rather than law.

- Employers’ liability insurance: Mandatory under the Employers’ Liability (Compulsory Insurance) Act 1969 if you employ any staff, including part-time workers. The legal minimum is £5 million, though most policies provide £10 million as standard.

- Trailer insurance: Covers owned or hired trailers against damage, theft, or third-party claims when detached from the tractor unit.

- Legal expenses cover: Funds the cost of pursuing or defending commercial disputes, licensing hearings, and contract disagreements.

- Breakdown cover: Provides roadside assistance and recovery for HGVs, reducing costly downtime on long-haul routes.

The value of a bundled haulage policy is that it consolidates these elements under a single renewal date and a single point of contact. Bundling coverages reduces administrative complexity and closes the gaps that arise when separate policies are managed independently.

Pro Tip: Always check whether your Goods in Transit policy covers temperature-controlled cargo separately. Standard GIT wording often excludes refrigerated or frozen goods unless a specific endorsement is added.

How does haulage insurance differ from courier or commercial vehicle insurance?

The distinction between haulage insurance and courier or standard commercial vehicle insurance is not merely technical. Using the wrong policy type can result in a total claim denial, leaving your business financially exposed.

The key differences are:

- Operating model: Haulage involves pre-planned, longer routes with fewer stops, typically carrying full loads between fixed origin and destination points. Courier operations involve multiple frequent drops across a local or regional area, creating a very different risk profile.

- Policy wording: Standard commercial vehicle policies generally exclude hire and reward operations, which is the legal basis on which haulage businesses carry goods for payment. A standard van policy applied to a haulage operation is effectively worthless when a claim arises.

- Cargo liability: Courier insurance is structured around high-frequency, lower-value parcel delivery. Haulage insurance addresses higher-value, single-consignment cargo with contractually stipulated liability limits.

- Vehicle class: Haulage policies are written for HGVs, articulated lorries, and rigid trucks. Courier policies typically cover vans and light commercial vehicles. The underwriting assumptions, premiums, and exclusions differ significantly between these classes.

The difference between haulage and courier insurance is most consequential when a claim is made. Insurers investigate the nature of the operation at the point of claim. If your declared use does not match your actual activity, the insurer can void the policy entirely.

Pro Tip: If your business carries out both haulage and courier-style multi-drop work, tell your broker. A combined or dual-use policy exists for this scenario and prevents the coverage gap that catches many operators out.

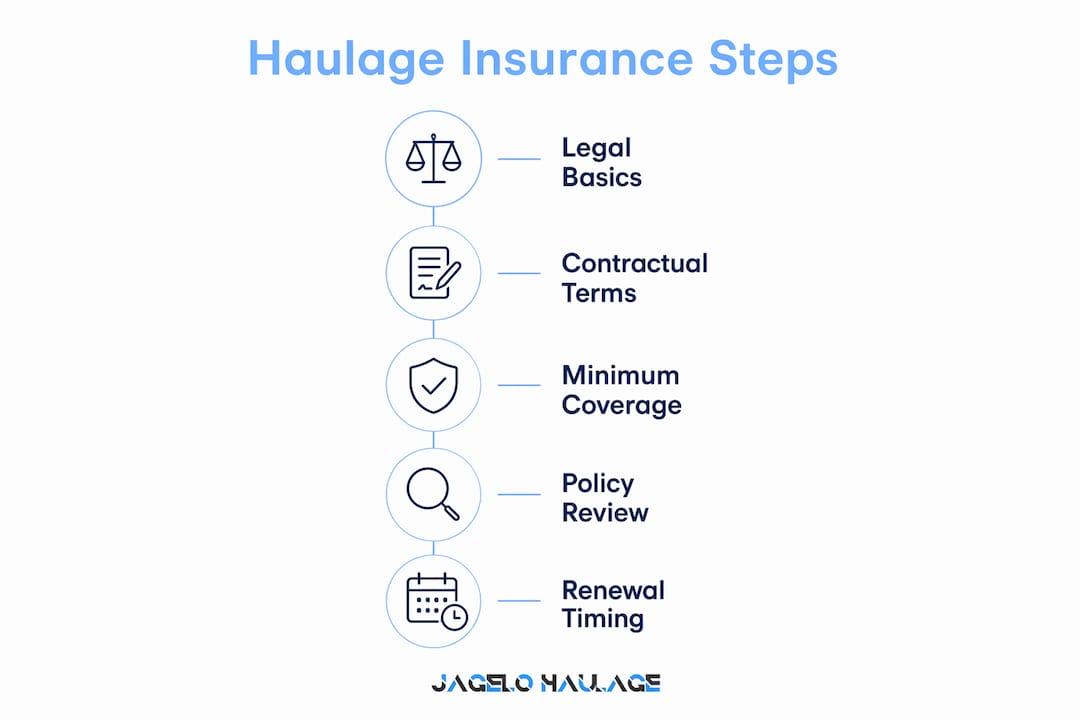

What are the legal and contractual insurance requirements for UK haulage operators?

UK haulage operators face two distinct sets of insurance obligations: those imposed by law and those imposed by commercial contracts. Both carry serious consequences if unmet.

| Requirement | Legal basis | Minimum level | Who sets it |

|---|---|---|---|

| HGV motor insurance | Road Traffic Act 1988 | Third-party liability | UK law |

| Employers’ liability | Employers’ Liability (Compulsory Insurance) Act 1969 | £5 million | UK law |

| Public liability | No statutory minimum | £1 million–£10 million | Customer contracts and site rules |

| Goods in Transit | No statutory minimum | Contractually defined | Customer contracts |

| Cargo liability limits | No statutory minimum | Contractually defined | Shipper or freight forwarder contracts |

The legal minimums represent the floor, not the ceiling. Liability insurance limits should be matched to the highest contract demand you face, not your average workload. A haulage operator working with a major retailer or port authority will typically face public liability requirements of £5 million or more. Failing to meet those thresholds means losing the contract.

Goods in Transit limits are almost always contractually mandated by the shipper or freight forwarder. If you carry high-value electronics, pharmaceuticals, or bonded goods, the cargo limit in your GIT policy must match or exceed the declared value of the consignment. A shortfall creates a personal liability gap that the business must absorb.

Policy wording also matters at the contractual level. Customers and site operators increasingly specify conditions such as overnight parking in approved locations, GPS tracking on vehicles, and named driver restrictions. If your policy contains these conditions and you breach them, insurers can deny claims even when the loss itself is genuine. Reviewing your haulage provider selection criteria alongside your insurance conditions is a sound practice before signing new contracts.

How to choose the right haulage insurance cover for your operations

Selecting the right haulage coverage options requires a structured assessment of your fleet, cargo, routes, and contractual obligations. There is no single policy that suits every operator, which is why specialist brokers exist in this market.

The following factors determine the shape of your cover:

- Fleet composition: The number of vehicles, their age, gross vehicle weight, and whether you operate articulated units, rigids, or a mixed fleet all affect underwriting. A fleet of 40 or more vehicles, such as those operated by Jhaulage, will be rated differently from a sole-operator setup.

- Cargo type: High-value, perishable, hazardous, or temperature-sensitive goods each carry distinct risk profiles. Your GIT policy must reflect the actual cargo you carry, not a generic description.

- Route profile: Regular international movements, overnight stops, or routes through high-theft areas require specific policy endorsements. Domestic port-to-door routes, such as those between Felixstowe, Tilbury, Southampton, and Liverpool, carry different risk characteristics from general domestic haulage.

- Contract requirements: Read every contract you sign for insurance clauses. Contractual cover limits are a key stumbling block for haulage operators and a common reason for losing contracts when insurance does not meet requirements.

- Driver vetting and security: Insurers frequently require documented driver vetting procedures, vehicle tracking, and approved overnight parking. Failing to maintain these conditions can void your cover at the worst possible moment.

Consolidating multiple coverages into a single haulage policy is the most practical approach for operators running more than two or three vehicles. It reduces the risk of gaps between policies and simplifies the renewal process considerably.

Pro Tip: Review your haulage insurance at every contract renewal, not just at annual policy renewal. A new customer contract may introduce liability limits or cargo conditions that your existing policy does not meet.

Key takeaways

Haulage insurance cover is a legally and commercially essential package that must be tailored to your fleet, cargo, routes, and contract obligations to provide genuine protection.

| Point | Details |

|---|---|

| Legal minimums are the floor | HGV motor insurance and £5 million employers’ liability are mandatory; contracts typically demand more. |

| GIT cover must match cargo value | Goods in Transit limits must equal or exceed the declared consignment value in every contract. |

| Wrong policy type voids claims | Standard commercial vehicle insurance excludes hire and reward; only specialist haulage policies apply. |

| Policy conditions must be followed | Breaching overnight parking, driver, or security conditions gives insurers grounds to deny valid claims. |

| Consolidate for coverage integrity | A single bundled haulage policy reduces gaps and simplifies administration across your fleet. |

Why I think most haulage operators underestimate their insurance exposure

Having worked closely with UK freight operators across container haulage, port logistics, and general road freight, the pattern I see most often is not deliberate negligence. It is a genuine misunderstanding of what haulage insurance actually covers and, more critically, what it does not.

The most costly mistake is assuming that a vehicle policy is a haulage policy. Using standard van or commercial vehicle insurance for hire and reward haulage trips can cause total denial of claims, leaving operators exposed to significant financial loss and operational disruption. I have seen operators lose everything on a single incident because their policy excluded the very activity they were carrying out.

The second issue is contractual complacency. Operators often secure a policy that meets the legal minimum and assume that is sufficient. Then a major shipper or port authority requests a certificate of insurance and the public liability limit falls short. That contract disappears. The fix is straightforward: set your liability limits to the highest demand you are likely to face, not the average.

The third issue is policy condition drift. A business grows, routes change, new drivers join, and overnight parking locations shift. The policy wording, however, stays fixed at the point of inception. Claims are frequently denied due to failure to adhere to policy wordings on factors like overnight parking locations, security equipment, and driver restrictions. An annual review of operational alignment with policy conditions is not optional. It is the difference between a policy that pays and one that does not.

— Vytautas

Jhaulage: insured container haulage across UK ports

Freight operators who need a haulage partner with documented insurance compliance and operational discipline will find Jhaulage a dependable choice.

Jhaulage operates a fleet of over 40 GPS-tracked trucks and trailers across the UK’s major container ports, including Felixstowe, Tilbury, Southampton, and Liverpool. Every movement is backed by appropriate haulage insurance cover, giving shippers and freight forwarders the compliance assurance their contracts demand. For businesses that need insured container haulage with 24/7 support and full port coverage, Jhaulage provides port-to-door services built around your supply chain requirements. Contact Jhaulage directly to discuss your container haulage and insurance compliance needs.

FAQ

What is haulage insurance cover in simple terms?

Haulage insurance cover is a package of policies protecting road freight businesses against vehicle damage, cargo loss, and liability claims. It combines legally required covers with commercially necessary protections into one policy.

Is goods in transit insurance a legal requirement in the UK?

Goods in Transit insurance is not a statutory requirement under UK law, but it is almost always required by customer contracts and freight forwarding agreements. Operating without it exposes your business to full financial liability for any cargo loss or damage.

What is the minimum employers’ liability insurance for haulage firms?

The Employers’ Liability (Compulsory Insurance) Act 1969 requires a minimum of £5 million in employers’ liability cover for any haulage business that employs staff. Most standard policies provide £10 million as a baseline.

Why do I need haulage insurance rather than standard van insurance?

Standard commercial vehicle insurance excludes hire and reward operations, which is the legal basis for carrying goods commercially. Using a standard policy for haulage work risks total claim denial and leaves your business without financial protection.

How often should I review my haulage insurance cover?

Review your haulage insurance at every contract renewal and whenever your operations change, including new routes, additional vehicles, or new cargo types. Policy conditions must remain aligned with actual operations to avoid claim disputes.

Recommended

- How haulage contracts work in the UK: 2026 guide | Jagelo Haulage

- Why Use an Insured Container Haulage Service | Jagelo Haulage

- A Comprehensive Guide to Merchant Haulage: How to Organise Efficient UK Container Transport | Jagelo Haulage

- Heavy Container Haulage: A Strategic Reference Guide for UK Logistics 2026 | Jagelo Haulage